This website use cookies for best experience. For more details read our Cookie Policy and Privacy Policy.

The 28th Regime (EU)

Updates, resources, and templates for Europe's planned optional company framework for innovative firms.

Europe is preparing an optional EU-wide "28th regime" for innovative companies. This site tracks what's official, what's proposed (EU-Inc.), and what founders and advisors should watch next.

Current status: The 28th regime is in legislative negotiation. Parliament's rapporteur put his draft report on the table on 29 June (PE790.143v01-00, 246 amendments); the JURI committee considered it on 15 July. In the Council, the Working Party met on 2 July, its first session under the Irish Presidency, with further sessions on 8 and 23 July. No final law yet.

On 15 July, JURI debated the draft report and the political groups split on the basics of the 28th regime. Our next newsletter maps where each group stands. Subscribe to get it.

Join the watchlist / newsletter (every ~2 weeks, free). Unsubscribe anytime.

Sign up to newsletterWhere to start

Pick the path that fits why you are here.

Following the file as an advisor, legal team, or policy professional.

Start with Progress for the timeline and primary documents, and Resources for institutional briefings and law-firm analyses.

New to the 28th regime and EU Inc.

Read the latest status below and the FAQ, then to see how EU-Inc., Regime-O, and the wider 28th regime differ check Compare proposals.

A founder or operator who expects to use EU Inc.

EU Inc. is still in negotiation and will not be usable for some time, so there is no rush. Some groundwork does not depend on the final text, and Templates & checklists sets out what is worth preparing now, including a free readiness checklist.

Updates come by newsletter, roughly every two weeks, free.

Why this matters

Scaling across the Single Market still means re-solving the same company setup, governance, and compliance problems country by country. That fragmentation acts like an "invisible tariff" on cross-border growth — the IMF has estimated persistent barriers in the EU Single Market are equivalent to a 110% tariff on services.

The "28th regime" is the idea of an optional EU-level rulebook that companies could choose, so operating across Member States becomes closer to "one set of rules" instead of 27 variations. The design details (scope, safeguards, and how it interacts with national labour/tax rules) will decide whether it becomes true simplification or a compromise layer.

This site tracks what's official, what's proposed, and what changes for founders the moment draft legal text lands.

Latest status

Last updated: 18 July 2026On 15 July, JURI debated the draft report, and the political groups divided over how far the 28th regime should reach: whether it stays open to all companies or is limited to start-ups, whether it remains a regulation on Article 114 or shifts toward an Article 50 directive, and whether it can bar public listing and exclude whole sectors. The progress tracker has the group-by-group breakdown, and our next newsletter maps where each group stands. Subscribe to get it.

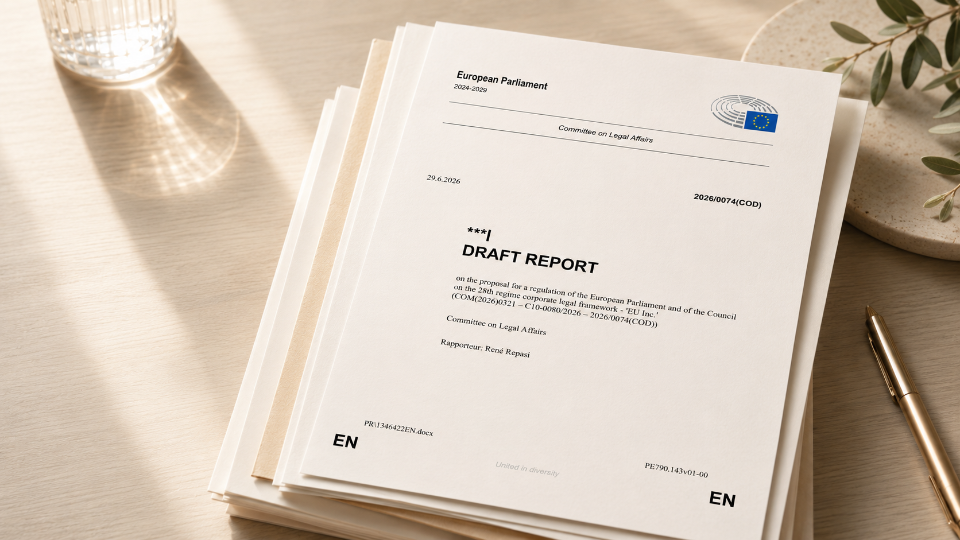

René Repasi's draft report on the 28th regime is dated 29 June 2026: reference PE790.143v01-00, 151 pages, 246 amendments to the Commission text. It is the rapporteur's opening rewrite, not yet the committee's position. The headline changes proposed: Article 4 (national law of the registration country as gap-filler) is deleted in favour of a labour-law firewall and designated national reference forms; eligibility becomes a numeric startup definition plus a list of excluded sectors (Annex Ia); public listing is banned outright; and two new options appear, a steward-owned variant (EU Inc. SO) and an employee stock ownership plan (EU-ESOP). The two-working-day, EUR 100 formation promise survives, subject to new identity and anti-fraud checks. Full analysis: inside the European Parliament's draft report.

Procedure: the political groups' amendments were due 17 July and are now with the committee, and ECON has delivered its opinion in the form of a letter (PE788.878, ECON Chair Aurore Lalucq, adopted 34 to 13 with 9 abstentions): it backs the proposal but wants EU Inc companies allowed to access public markets and an optional tax module added. JURI takes up the amendments on 7 September; the committee vote is expected in September (tbc) and the plenary in October (tbc).

In the Council, Ireland took over the Presidency on 1 July with the 28th regime named in its programme. Session 10 of the Working Party on Company Law, the first under the Irish chair, met on 2 July; Session 11 met on 8 July; Session 12 follows on 23 July. For the full legislative timeline and source links, see progress.

Draft report PE790.143v01-00, Committee on Legal Affairs, 29 June 2026.

Previous status

Last updated: 27 June 2026On 28 May, COMPET ministers held the first minister-level debate on the 28th regime. The signal was momentum, not agreement on text: safeguards, legal certainty, labour rules, tax, insolvency, and the Article 114 legal-basis question all remain open. Twenty-six delegations spoke; the first public country groupings are now visible. For the full breakdown, read our analysis of the first public country positions.

Council technical work continues. Sessions 6, 7, 8, and 9 were held on 2, 11, 17, and 25 June respectively. Session 7 (agenda CM-3040/26, Europa Building) took the formation and governance chapter (Articles 35 to 58), with Parliament's Employment Committee (EMPL) present — the most politically sensitive chapter so far, covering codetermination and worker board representation. No public readout has appeared from any session. Further confirmed meetings on 2, 8, and 23 July continue under the Irish Presidency, which takes over on 1 July.

In Parliament, René Repasi (S&D, Germany) is rapporteur for the file. His draft JURI report is expected on 26 June, the first text-level EP position on the file. Axel Voss (EPP, Germany/CDU) is now confirmed as the EPP shadow rapporteur. Amendments are due on 17 July; the committee vote is expected in September (tbc); plenary vote (tbc). If agreement is reached by end of 2026, the regime is expected to be operational from early 2027.

For the full legislative timeline and source links, see progress.

COMPET ministerial debate on EU Inc., 28 May 2026.

Previous status

Updated: 22 May 2026Five Working Party sessions had been held since March, with Session 5 on 18 May the most recent. No public readout from any session had appeared on the Council register. The compound readout for Sessions 3-5 was expected to surface around or after the COMPET ministerial meeting.

The 28-29 May COMPET ministerial Council had EU Inc. confirmed as item 2 on the 28 May agenda, under public deliberation rules. That made it the first formal minister-level debate on the proposal. Ireland was due to present its incoming Presidency work programme at the close of both days, confirming the legislation would continue into H2 2026.

In Parliament, the rapporteur for procedure 2026/0074(COD) was still pending. Commissioner McGrath had presented the proposal to JURI, Parliament's Legal Affairs Committee, on 4 May. Later Working Party sessions were scheduled for 2 June and 17 June.

For a detailed look at what the 7 May ECGI, Bocconi, and LawFin workshop surfaced about EU Inc.'s legal design, read our editorial report from the 7th LawFin Workshop.

.jpg)

Lex building, Brussels.

Photo: Trougnouf (Benoit Brummer), CC BY 4.0, via Wikimedia Commons.

Previous status

Updated: 29 Apr 2026Three Council Working Party sessions have now been held — 23 March, 17 April, and 27 April — and no public readout or outcome note is visible from any of them. The next institutional milestones are the JURI Committee meeting on 4 May and the two-day Council Session 4 on 6–7 May, with further Council sessions already listed for 18 May and 2 June. The file is under steady technical examination, but the schedule is now more informative than the readouts.

The European Parliament's JURI Committee — Parliament's Legal Affairs Committee — has still not named a rapporteur. Commissioner McGrath presents the proposal to JURI on 4 May, and the rapporteur is expected at or shortly after that meeting. If you want the plain-language version of who does what, see what JURI is and what the rapporteur does.

The most substantive public debate so far happened on 21 April, when the EESC Workers' Group and the ETUC held a full-day conference titled "28th Regime — Why are alarm bells ringing?" Commissioner Michael McGrath said competitiveness cannot come from weaker worker protection, and MEP Rene Repasi warned that a regime with too many routes for abuse could damage the project before it proves itself. The central unresolved question from the conference: how collective rights — bargaining, board representation — are governed when a company registers in one member state but operates mainly in another.

One practical follow-on from the late-April newsletter: readers were especially interested in the April EPRS briefing on the proposal. It is still the clearest short institutional summary of the legal route behind EU Inc. — why the Commission chose a Regulation under Article 114 TFEU, where Parliament's earlier position pointed to Articles 50 and 114 together and preferred a Directive, and why that treaty choice matters.

For the full timeline and primary docs, including the EPRS note, see progress. For the plain-language explainer of JURI, the rapporteur, trilogue, and Article 114, see JURI, rapporteur, trilogue, and Article 114 in the FAQ. For the late-April coverage, see the EESC debate on EU Inc and worker protection.

Michael McGRATH, Commissioner for Democracy, Justice, the Rule of Law and Consumer Protection — video message, EESC Workers' Group conference, 21 April 2026.

Excerpt on YouTube ·

Morning session ·

Afternoon session ·

Programme

© European Union, 2026. Source: European Economic and Social Committee (EESC)

Previous status Updated: 21 Mar 2026

On 19 March 2026, the European Council endorsed the "One Europe, One Market" agenda and named the 28th regime for company law as a priority measure for 2026. Leaders called on the co-legislators to adopt it by the end of 2026, on the basis of the Commission proposal of 18 March. Antonio Costa confirmed at the post-summit press conference that the timeline is end of 2027 but mostly this year, in 2026.

No new legal text was published. The only legal text remains the Commission proposal of 18 March. What changed is the political level: EU Inc. is now an endorsed European Council priority with a deadline.

Full stored update: EU leaders back EU Inc - from proposal to political priority.

Previous status Updated: 18 Mar 2026

The European Commission has now published the EU Inc. proposal together with the wider 28th-regime package: the Communication, the draft corporate framework, the annex, factsheet, and impact-assessment papers. This is the real shift from expectation to text - the debate can now move from whether the proposal will appear to what the legal text actually creates, what is still missing, and what may change in the legislative process.

The core offer is an optional EU-wide company framework designed to make incorporation and cross-border operation simpler: faster digital registration, lower setup costs, digital-by-default procedures, easier share transfers, digital insolvency, and an EU-level stock-option approach aimed at making startups and scaleups easier to build and finance in Europe.

Full stored update: EU Inc. Proposal Explained: What the Official Documents Actually Say.

Previous status Updated: 24 Feb 2026

Parliament's tax subcommittee (FISC) held a public hearing on the feasibility of a "28th tax regime" - a clear sign that tax barriers and incentives are now being discussed alongside the upcoming EU-Inc / 28th-regime corporate proposal. Three expert groups (Bruegel, CEPS, ETAF) presented directions; the common ground was a narrow, practical scope focused on equity and stock-option treatment and administrative simplification rather than broad tax harmonisation.

The hearing surfaced three distinct approaches - Bruegel argued for a targeted digital hub with equity taxation at sale (not at grant) as the key lever; CEPS proposed modular tax-interoperability layers (loss relief, mobility rules, VAT and withholding simplification) added gradually on top of the corporate-law base; ETAF supported single-entry reporting but warned that substantive tax changes trigger Council unanimity and risk adding parallel complexity. The rapporteur, Ludovit Odor, pushed throughout on whether the regime needs a tax element to be attractive in practice - MEPs converged on digital-by-default setup, tax neutrality for opting in, and a credible fix for stock-option treatment as the realistic minimums.

Stored in the newsletter archive.

Previous status Updated: 15 Feb 2026

The European Parliament has formally adopted recommendations supporting a harmonised 28th regime for innovative companies, including fast digital incorporation and cross-border operation features; this feeds into the European Commission's upcoming legislative work.

What's changed is timeline clarity: the European Parliament's Legislative Train tracker currently lists the Commission proposal as scheduled for 18 March 2026. We're also monitoring for publication before the March European Council (19-20 March 2026). Note: scheduled means planned, not guaranteed - calendars can slip.

Political framing is now explicit: President von der Leyen is packaging EU-Inc / 28th regime inside a One Europe, One Market roadmap with five building blocks - where pillar 2, build one market, is the relevant lane for this initiative, alongside deeper capital markets. The ambition is framed as reaching One Europe, One Market by end-2027.

Stored in the newsletter archive.

Previous status Updated: 26 Jan 2026

The European Parliament has formally adopted a set of recommendations supporting a harmonised 28th regime for innovative companies, including digital incorporation and cross-border operation features; this will feed into the European Commission's legislative proposal expected in Q1 2026.

At the World Economic Forum, Commission President Ursula von der Leyen publicly backed the initiative under the EU-Inc banner. Discussions now hinge on the regime's design, regulation versus directive, and social safeguards.

Stored in the newsletter archive.

What you'll find on this site

A neutral trackerA dated changelog of official milestones, plus what each step actually means for founders, investors, and operators.

A curated libraryThe best primary docs and a small number of high-signal explainers — no clutter.

Clear comparisons (with receipts)One page that compares what proposals actually say on scope, governance, registry model, ESOP/tax principles, dispute resolution, and more.

Templates & checklists Checklists and decision tools for EU Inc. preparation.

Get updates

Stay ahead of the changes, subscribe

Sign up to receive updates up to twice a month.

Only 1 more step!

Please check your inbox to confirm your subscription!

We just sent you the email with a confirmation link. Confirm by clicking on it to activate the subscription. - adin@the28thregime.eu

PS: also check your SPAM folder

* Independent project. Not affiliated with EU institutions. Not legal advice.

We may add partner links later; if we do, we’ll label them clearly.